Is The First Time Home Buyer Incentive Helping The Canadian Economy?

Is The First Time Home Buyer Incentive Helping The Canadian Economy?

Latest on Canadian Real Estate Market Trends by Steve Saretsky,

September 16, 2019

Happy Monday Morning!

Falling further into the abyss, the European Central Bank slashed interest rates deeper into negative territory, forcing them down from -0.4% to -0.5%. The ECB also announced the re-introduction of their Quantitative Easing program, which will soak up $20 billion euros per month of net asset purchases for as long as it deems necessary. ECB president Mario Draghi, solidified his tenure at the Bank going from ‘whatever it takes’ to ‘However long it takes.’ President Draghi didn’t hold any punches as to the future outlook of interest rates, “We now expect the key ECB interest rates to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2%.” Concluding, “Negative rates will not provoke the collapse of the financial system.”

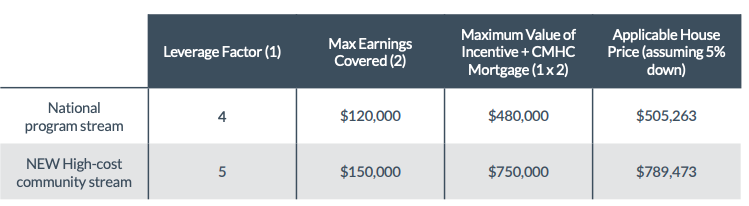

Across the pond, Canadian politicians are gearing up for a federal election here in October, and they come bearing promises and stimulus of their own making. Prime Minister Justin Trudeau announced the taxpayer funded First Time Home Buyer Incentive will be expanded in Vancouver, Victoria, and Toronto to include a first time purchase up to $789,000. The revised program will allow first time buyers in these frothy cities to increase leverage from 4:1 to 5:1.

In other words, as per Rate Spy, under the old scheme, many FTHBI users could buy a more expensive home if they opted for a regular old insured mortgage. Now, FTHBI users could qualify for just as much as non-FTHBI users, often more. In fact, a couple with the minimum down and making $150,000 with no other debt could now afford roughly $40,000 more home by using the FTHBI.

If they bought a new-build, where the government incentive is doubled (i.e., 10% of the purchase price), borrowers could afford an even higher-priced home. It doesn’t take a PhD to determine this is terrible economics, but it is at least a reminder that short term politics prevail over longer term sustainability.

Speaking of politics, the Liberal Government pulled one out of the BC NDP’s housing playbook, adding they too would bring in a 1% annual vacancy and speculation tax on applicable residential properties owned by non-resident and non-Canadians. “This would be modelled at a national level on B.C.’s successful speculation and vacancy tax. Canadians who live abroad, as well as non-Canadians who live in Canada, will not be affected in any way. This tax will be administered by the Canada Revenue Agency (CRA) and will apply in addition to any local taxes that non-resident, non-Canadian owners may already be subject to.”

With housing once again taking front and centre in the upcoming elections, it is expected Conservative leader Andrew Scheer will respond with his own counter-proposals later this week. Hold your breath as the nations most important fundamental asset hangs in the balance, swayed by policy making on the fly.

Three Things I’m Watching:

1. Liberal Government proposes increased leverage to first time home buyer incentive program in Vancouver, Victoria and Toronto.

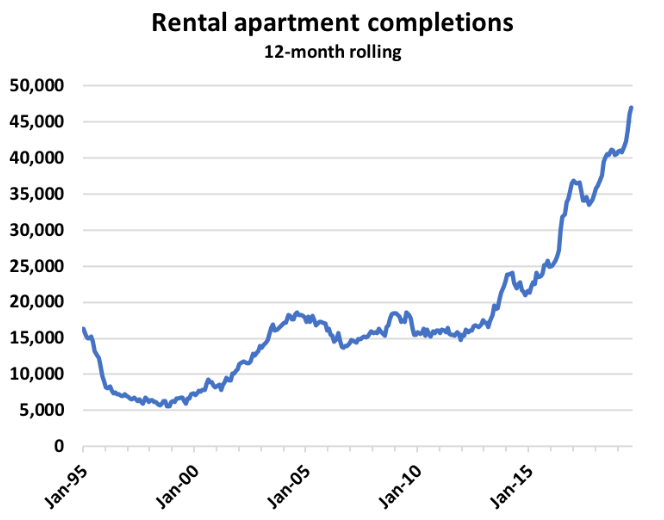

2. Rental apartment completions are surging across Canada.

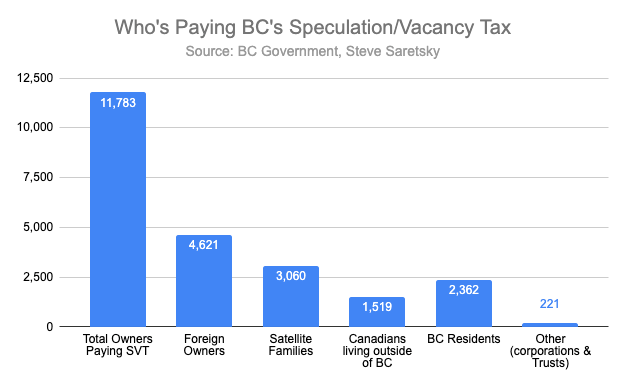

3. Per BC Government data, Canadians & BC Residents make up 33% of total home owners paying the speculation/ vacancy tax introduced earlier this year.